Top 5 Mistakes HNWI Make With Their Finances

Thomas Rogerson, Wealth Management Director at Pyrmont Wealth, has helped high-net-worth individuals (HNWI) make the most of their life and finances for over the past decade. A dual-licensed (UK and HK) expert financial planner who works with busy, successful, individuals and families, that are looking for clarity, simplification and structure with their financial planning and wealth management, reveals some of his top observations from working with numerous expats in Hong Kong.

This week, we caught up with Tom to discuss the Top 5 Mistakes High-Net-Worth Individuals (HNWI) Make With Their Finances.

Thomas Rogerson, Director Wealth Management

-

Not taking on enough risk

“First off let me clarify on the ambiguous title; when I say not taking on enough risk, I don’t mean not buying enough bitcoin, or not putting enough money into that Australian mining stock your friend told you is going to go up 10x.

The biggest mistake we see with new HNWI clients, often regardless of whether they had an existing advisor or not, is holding too much cash, and/or being too conservative with their portfolio.

In this instance, inflation and opportunity cost (missing out on higher returns on offer elsewhere) are two of the biggest barriers to building long-term wealth and achieving the life you want.

Another handful will be super adventurous, but being acutely aware of this risk, they are only laying a few chips on the table, and therefore whether the investment goes to the moon or to zero, will have little material impact on their long-term wealth.

We work with clients to establish a well thought out financial plan. Once we have analysed their current financial position, capacity for accumulating further assets and understanding how they want their future to look (you could read this as goals…), we can then build a personalised investment portfolio.

This portfolio recommendation will first ensure they have enough cash so that they can sleep at night without worrying about what might happen if something nasty pops up unexpectedly (job loss, car breakdown, emergency travel needs etc).

The remainder will then be systematically allocated to the appropriate proportion of stocks and bonds to offer the best chance of success for the client in question. Taking on enough risk to ensure they are adequately rewarded by the market, but not so much that it could jeopardise the plan.”

-

Lack of Smart Diversification

“Here I added the word “smart” to cover off two issues in one, as again there are often two issues we see.

The first is a plain lack of diversification, often referred to as “putting all of your eggs in one basket”!

This can take a few forms:

- Being overly invested into a single company (often your employer); putting you and your financial future at extreme risk if just one single company collapses. We’ve seen this numerous times, think Lehman Brothers, Enron or even WeWork after a failed IPO.

- Some investors might have multiple holdings, but all in similar industries (e.g. Technology). When that part of the market crashes, there are rarely any stocks which escape. Holding 15 or 30 tech stocks during the dot com crash would not have served you any better than holding 1.

The second common issue we see is investors holding multiple different funds, often with different advisors, and feeling like they are well diversified. However, with the lack of a single, coordinated portfolio management approach, the benefits can often be diluted. More often than not, this approach just leads to duplication of holdings within the funds, increased costs, and in turn lower returns.

Which brings us nicely on to the next mistake.”

-

Failure to fully understand the true cost of investing

“Increased costs ultimately lead to lower returns, as the sum of all market participants will achieve the return of the market minus costs and charges.

The chart below shows us that for US equity (stocks/shares) funds, as expense ratios (the total cost of an investment fund) increase, the number of funds which outperform their benchmark decreases.

For example, over the last 20 years, only 6% of funds with a ‘High’ expense ratio beat their benchmark, compared with 31% of those funds with a ‘Low’ expense ratio.

In other words, paying more in management fees does not offer more in return.

Costs are one of the few things we can control, so having a handle on this is vital. Many clients who come to us with existing investments, products, and services, are not fully aware of how much they are paying away in fees and charges. We frequently come across clients whose costs are far in excess of 2% per year.”

-

Being susceptible to Fear-Of-Missing-Out (FOMO)!

“We touched upon this at the start; that mining stock your friend mentioned; the wife’s co-worker’s brother’s friend who made $20MM from Dogecoin; that new fund your new RM at the bank who wants to be your best friend is trying to flog you, based on its past 3 years returns…

These are all preying on your fear of missing out, chasing trends and trying to invest in the next big thing.

How many times have you seen the phrase “Past Performance is no guarantee of future results”? Heck, it’s even in the footnotes of this blog!

This phrase is the most (probably) used compliance term for a reason, and yet it is also one of the most ignored pieces of advice by both prospective clients and clients alike: One research study found that 39% of all new investment into mutual funds went into the 10% of funds which had the best performance the previous year.[ii]

Thankfully our existing clients often use us as a sounding/sense check board before making any decision to invest on this emotional bias.”

-

Trying to time the market

“Finally, we come to perhaps one mistake that is perhaps the most common destroyer of wealth for HNW investors.

Mistake number 3 alludes to the fact that even the professionals, charging higher management fees, cannot effectively beat the market by timing or stock selection. And yet so many people continue to try and do this.

This is arguably a combination of all of the previous 4 mistakes rolled into one. Taking on too much/too little risk at the wrong times, trying to tactically allocate to move with the market, trading in and out of the market too frequently incurring additional cost, and trying to pick outperformers.

The result of this is that investors end up under compensated for allocating their capital to the markets.

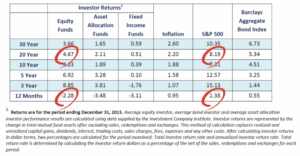

A 2016 study by Dalbar looked at the US stock market (S&P 500) returns, compared with the returns of the average investor into US stock funds. We can see that over the 20-year period the average investor ended up with just 4.67% per year return, compared with the market, buy and hold return of 8.19%.

Assuming a $500,000 investment to begin with, these mistakes along the way cost the average investor over $1.1MM in lost return.”

Summary

“Without doubt, our most valuable role as a trusted advisor to HNW clients, is to manage their behaviour and coach them to be better investors.

This results in our clients receiving the returns they are entitled to from the market for taking on risk with their capital.

The real upshot and benefit of that, is that clients can achieve their goals and live the life that they dream of.”

Contact Us

We are here to help you avoid these mistakes and more. Contact us to learn how you we can help you create a wealth of possibilities with your life and money.

[i] Source: Dimensional 2022.

The sample includes funds at the beginning of the 20-year period ending December 31, 2021. Each fund is evaluated relative to its primary prospectus benchmark. Survivors are funds that had returns for every month in the sample period. The sample includes US-domiciled funds at the beginning of the 10-, 15-, and 20-year periods ending December 31, 2021. Funds are sorted into quartiles within their category based on average expense ratio over the sample period. The chart shows the percentage of winner and loser funds by expense ratio quartile for each period. Winners are funds that survived and outperformed their benchmark over the period. Losers are funds that either did not survive or did not outperform their respective benchmark. All rights reserved. Indices are not available for direct investment. Their performance does not reflect the expenses associated with management of an actual portfolio. US-domiciled mutual funds and US-domiciled ETFs are not generally available for distribution outside the US. There is no guarantee investment strategies will be successful. Past performance is no guarantee of future results.

[ii] Jain Prem C. and Joanna Shuang Wu. “Truth in mutual fund advertising: Evidence on future performance and fund flows.” The Journal of Finance, vol. 55, oo. 2, 2002, pp. 937-958.